Samco Trade API Documentation v2.0

Scroll down for code samples, example requests and responses. Select a language for code samples from the tabs above or the mobile navigation menu.

Samco Trade API is a set of Rest APIs using which users can build customized applications based on their trading requirements. It facilitates the users of the APIs to login, search symbols, place orders and execute them, view their order status, positions and holdings etc. This documentation provides you with all the necessary details to understand the Samco StockNote API collection. APIs are compatible with both Javascript and Python.

For any issues or support, please raise ticket to us using the support link and we will be happy to assist you.

For Reference you can download postman collection Click here

For downloading a list of all tradeable scrips across exchanges please Click here This is a CSV file which you can import into your database.

If you are using Python,Java or JavaScript as client platform to code your strategies and integrate with our APIs, you can use our StockNoteBridge which provides pre-written wrappers over StockNote APIs that ensure seamless and reliable connectivity to the APIs and help you fast-track your development process.

| Languages | Documentation |

|---|---|

| Python | Python SDK Documentation |

| Java | Java SDK Documentation |

| JavaScript | NodeJS SDK Documentation |

Add 'session token' of login api response as 'x-session-token' in header param of all Apis.

NOTE: To ensure stability and there by provide seamless services to our customers, Samco may set limits on your use of the Trade APIs (for example, limit on the number of requests sent to a specific API) . If you have additional questions regarding the rate limits on APIs, please reach out to us using the support link and we will be happy to assist you.

Supports the list of following index names:

| BSE CG | SENSEX | BSE CD | NIFTY50 PR 1x INV |

| BSE IT | METAL | OILGAS | NIFTY50 PR 2x LEV |

| BSEIPO | GREENX | POWER | NIFTY50 TR 1x INV |

| CARBON | BASMTR | CDGS | NIFTY50 TR 2x LEV |

| BSEFMC | BSE HC | ALLCAP | NIFTY50 TR 2x LEV |

| REALTY | SMEIPO | DOL30 | NIFTY Mid LIQ 15 |

| LRGCAP | MIDSEL | SMLSEL | NIFTY100 LIQ 15 |

| SNXT50 | SNSX50 | NIFTY 50 | NIFTY Quality 30 |

| NIFTY BANK | NIFTY NEXT 50 | DOL100 | NIFTY MIDCAP 50 |

| NIFTY 100 | NIFTY 200 | NIFTY 500 | NIFTY FIN SERVICE |

| NIFTY AUTO | NIFTY FMCG | NIFTY IT | NIFTY COMMODITIES |

| NIFTY MEDIA | NIFTY METAL | NIFTY PHARMA | NIFTY CONSUMPTION |

| NIFTY PSU BANK | NIFTY PVT BANK | NIFTY REALTY | NIFTY GROWSECT 15 |

| NIFTY CPSE | NIFTY ENERGY | NIFTY INFRA | NIFTY DIV OPPS 50 |

| NIFTY MNC | NIFTY PSE | NIFTY SERV SECTOR | NIFTY MID100 FREE |

| DOL200 | TECK | BSEPSU | NIFTY SML100 FREE |

| AUTO | BANKEX | INDIA VIX | NIFTY50 VALUE 20 |

APIs will work intermittently over the weekends/holidays and outside market hours due to maintenance activity. Base URLs:

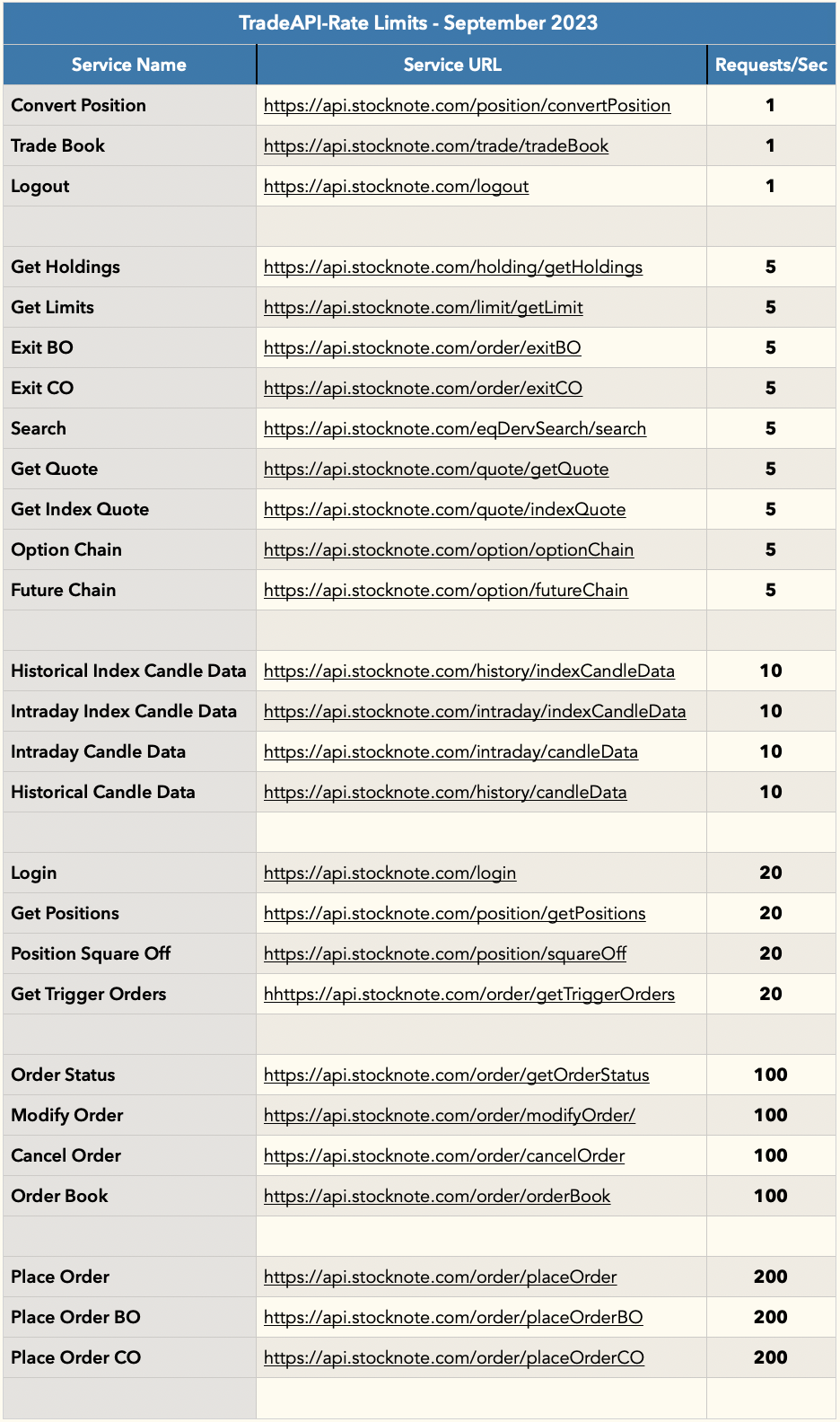

Trade Limits

Rate Limits - September 2023

Our Samco Trade APIs are set with defined rate limits, which are based on the IP address. If these limits are exceeded, a "429 - Too Many Requests" error may occur. We've recently updated our rate limit policy, which involves enhancing the limits for specific Samco APIs.

Updated list of our API request limits and time limits:

User Login

User Login

Code samples

var headers = {

'Content-Type':'application/json',

'Accept':'application/json'

};

$.ajax({

url: 'https://api.stocknote.com/login',

method: 'post',

data: JSON.stringify(requestBody),

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Content-Type': 'application/json',

'Accept': 'application/json'

}

r = requests.post('https://api.stocknote.com/login'

, data=json.dumps(requestBody)

, headers = headers)

print r.json()

POST /login

The Samco Trade APIs allow the user authentication using the Login API. A valid Samco Trading Account and subscription to Trade API Services is a pre-requisite for successful authentication. For Example, if you are going to use 3 users for Trading using APIs, all the 3 users will have to open a Samco Trading Account and will have to subscribe to Samco Trade API Services.

Body parameter

requestBody={

"userId": "DV99999",

"password": "abc1234",

"yob": "1975"

}

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| body | object | false | none |

| userId | string | true | The client Code provided to you by SAMCO after opening an account. |

| password | string | true | If user has set password using any of the SAMCO Trading platform i.e. Stocknote Mobile App, Stocknote Web or Stockbasket, then use the password as set. Or else, use the password provided in the welcome email sent to you at the time of account opening. |

| yob | string | true | Your year of birth. |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Request successful",

"sessionToken": "078131a2d0d5877ecbf2a130e16acd78",

"accountID": "DV99999",

"accountName": "FirstName LastName",

"exchangeList": "NFO,NSE,CDS",

"orderTypeList": "L, MKT, SL",

"productList": "CNC, CO, MIS,NRML"

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Login Successful. Session token, which is used as authenticator for all requests after login is generated after successful login. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error.Login failure. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Login Success or Failure. |

| statusMessage | string | status Message |

| sessionToken | string | Session token that should be used with API request is given in the response. It is used as an authenticator. A session token is valid for 24 hours or until a new login request is given, where you a new session token will be generated and the previous one will get expired. |

| accountID | string | Same as Client Code for SAMCO Trading Account, is unique and used for identification of user. |

| accountName | string | Users full name as registered with Samco Trading Account. |

| exchangeList | [string] | List of exchanges enabled for trading for the user. |

| orderTypeList | [string] | List of order types enabled for trading for the user.The list can be from of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| productList | [string] | List of product types enabled for the user . It can be CNC (Cash and Carry),BO (Bracket Order),CO (Cover Order),NRML (Normal),MIS (Intraday). |

Search Equity & Derivative

Search Equity scrips

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'115aead43798e35cef8308c15cc79c7a'

};

$.ajax({

url: 'https://api.stocknote.com/eqDervSearch/search?searchSymbolName=INFY',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': '115aead43798e35cef8308c15cc79c7a'

}

r = requests.get('https://api.stocknote.com/eqDervSearch/search', params={

'searchSymbolName': 'INFY'

}, headers = headers)

print r.json()

GET /eqDervSearch/search

This API is used to search equity, derivatives and commodity scrips based on user provided search symbol and exchange name.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| exchange | string | false | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| searchSymbolName | string | true | Trading Symbol of the scrip to be searched |

Example responses

200 Response

{

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Request successful",

"searchResults": [

{

"exchange": "NSE",

"scripDescription": "INFOSYS LIMITED",

"tradingSymbol": "INFY-EQ",

"isin": "INE009A01021",

"bodLotQuantity": "string",

"tickSize": "0.05",

"instrument": "FUTIDX",

"quantityInLots": "10"

}

]

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Scrip details successfully retrived. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to retrieve scrip details. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| searchResults | [object] | Scrips Details available for the provided search text. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| scripDescription | string | scrip description |

| tradingSymbol | string | Trading Symbol of the scrip. |

| isin | string | The standard ISIN representing stocks uniquely at international level. It is same for every exchange. |

| bodLotQuantity | string | none |

| tickSize | string | The value of a single price tick. Default value is 0.05 |

| instrument | string | Instrument Name. |

| quantityInLots | string | Lot size of the symbol to be traded. At the time of placing order, the quantity should be in multiples of Broadlot Qty only. |

Quote

Index Quote

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/quote/indexQuote?indexName=Sensex',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/quote/indexQuote', params={

'indexName': 'Sensex'

}, headers = headers)

print r.json()

GET /quote/indexQuote

Getting Index Quote details for a specific Indicies. This helps user with market picture of an specific Index Details.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| indexName | string | true | Index name of the scrip. |

Example responses

200 Response

{

"serverTime": "23/07/20 11:05:43",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Index Quote details retrieved successfully.",

"indexName": "Sensex",

"listingId": -101,

"lastTradedTime": "23/07/2020 11:05:39",

"spotPrice": 38015.28,

"changePercentage": 2.05,

"averagePrice": 1586.5,

"openValue": 37871.52,

"highValue": 37871.52,

"lowValue": 37871.52,

"closeValue": 37871.52,

"totalBuyQuantity": 0,

"totalSellQuantity": 0,

"totalTradedValue": 0,

"totalTradedVolume": 0,

"change": 13.57

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Index Quote details retrieved successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to get Index details. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | Status message of the Quote request |

| indexName | string | Index Name of the indices. |

| listingId | string | Identifier assigned to the scrip by exchange in the format <>_<> |

| lastTradedTime | string | Time of the last transaction |

| lastTradedPrice | string | Price at which last transaction / trade is done |

| spotPrice | string | Spot price. Applicable in case of Futures and Options |

| changePercentage | string | Percentage of change between the current value and the previous day's market close |

| lastTradedQuantity | string | Quantity of last transaction |

| averagePrice | string | average price of a market snapshot |

| openValue | string | Opening price of a market snapshot |

| highValue | string | High value of market snapshot |

| lowValue | string | Low value of market snapshot |

| closeValue | string | Close value of market snapshot |

| totalBuyQuantity | string | Total quantity of BUY transaction |

| totalSellQuantity | string | Total quantity of SELL transaction |

| totalTradedValue | string | Value of total trade made for the scrip |

| totalTradedVolume | string | Total volume of trading done |

| openInterest | string | Open interest is the Number of existing contracts held by buyers or sellers for any market for any given day. |

| getoIChangePer | string | It will shows the change % based on Open Interest |

Get Quote

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/quote/getQuote?symbolName=RELIANCE',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/quote/getQuote', params={

'symbolName': 'RELIANCE'

}, headers = headers)

print r.json()

GET /quote/getQuote

Get market depth details for a specific equity scrip including but not limited to values like last trade price, previous close price, change value, change percentage, bids/asks, upper and lower circuit limits etc. This helps user with market picture of an equity scrip using which he will be able to place an order.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| exchange | string | false | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| symbolName | string | true | Symbol name of the scrip.For Equity enter SymbolName of the scrip & For Derivatives enter TradingSymbol of the scrip |

Example responses

200 Response

{

"serverTime": "15/10/19 17:27:43",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Quote details retrieved successfully.",

"symbolName": "RELIANCE",

"tradingSymbol": "RELIANCE",

"exchange": "NSE",

"companyName": "RELIANCE INDUSTRIES LTD",

"lastTradedTime": "03/12/2019 12:05:39",

"lastTradedPrice": "1600.00",

"previousClose": "1456.90",

"changeValue": "143.10",

"changePercentage": "9.82",

"lastTradedQuantity": "1",

"lowerCircuitLimit": "1427.85",

"upperCircuitLimit": "1745.15",

"averagePrice": "1599.29",

"openValue": "1586.50",

"highValue": "1600.00",

"lowValue": "1575.50",

"closeValue": "1456.90",

"totalBuyQuantity": "50092",

"totalSellQuantity": "49421",

"totalTradedValue": "9.6437187 (Lacs)",

"totalTradedVolume": "603",

"yearlyHighPrice": "1614.45",

"yearlyLowPrice": "1055.00",

"tickSize": "0.05",

"openInterest": "5",

"bestBids": [

{

"number": "2",

"quantity": "88",

"price": "1575.55"

}

],

"bestAsks": [

{

"number": "2",

"quantity": "88",

"price": "1575.55"

}

],

"expiryDate": "26 Dec, 2019 - 14:30:0",

"spotPrice": "1578.35",

"instrument": "EQ",

"lotQuantity": "500",

"listingId": "2885_NSE",

"openInterestChange": "285500",

"getoIChangePer": "13.57"

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Successfully retrived market depth details for the input scrip. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to get market depth of scrip. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | It would be success or failure |

| statusMessage | string | Status message of the Quote request |

| symbolName | string | Symbol name of the scrip. |

| tradingSymbol | string | Trading Symbol of the scrip. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| companyName | string | Full name of the company |

| lastTradedTime | string | Time of the last transaction |

| lastTradedPrice | string | Price at which last transaction / trade is done |

| previousClose | string | Previous close refers to the prior day's final price of a security when the market officially closes for the day |

| changeValue | string | Change value is the difference between the current value and the previous day's market close |

| changePercentage | string | Percentage of change between the current value and the previous day's market close |

| lastTradedQuantity | string | Quantity of last transaction |

| lowerCircuitLimit | string | Limit below which a stock price cannot trade on a particular trading day |

| upperCircuitLimit | string | Limit above which a stock price cannot trade on a particular trading day |

| averagePrice | string | Average price of the trading |

| openValue | string | Opening price of a market snapshot |

| highValue | string | High value of market snapshot |

| lowValue | string | Low value of market snapshot |

| closeValue | string | Close value of market snapshot |

| totalBuyQuantity | string | Total quantity of BUY transaction |

| totalSellQuantity | string | Total quantity of SELL transaction |

| totalTradedValue | string | Value of total trade made for the scrip |

| totalTradedVolume | string | Total volume of trading done |

| yearlyHighPrice | string | 52 week high |

| yearlyLowPrice | string | 52 week low |

| tickSize | string | The value of a single price tick. Default value is 0.05 |

| openInterest | string | Open interest is the Number of existing contracts held by buyers or sellers for any market for any given day. |

| bestBids | [object] | Most frequent trading bids for BUY |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

| bestAsks | [object] | Most frequent trading asked for SELL |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

| expiryDate | string | Expiry date of the scrip |

| spotPrice | string | Spot price. Applicable in case of Futures and Options |

| instrument | string | Instrument Name. |

| lotQuantity | string | Lot quantity. Applicable for F & O |

| listingId | string | Identifier assigned to the scrip by exchange in the format <>_<> |

| openInterestChange | string | It shows Open interest change in Number of contracts held for market |

| getoIChangePer | string | It will shows the change % based on Open Interest |

Option

Option Chain

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'115aead43798e35cef8308c15cc79c7a'

};

$.ajax({

url: 'https://api.stocknote.com/option/optionChain?searchSymbolName=TCS',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': '115aead43798e35cef8308c15cc79c7a'

}

r = requests.get('https://api.stocknote.com/option/optionChain', params={

'searchSymbolName': 'TCS'

}, headers = headers)

print r.json()

GET /option/optionChain

This API is used to search OptionChain for equity, derivatives and commodity scrips based on user provided search symbol and exchange name.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| exchange | string | false | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| searchSymbolName | string | true | Trading Symbol of the scrip to be searched |

| expiryDate | string | false | From date in yyyy-MM-dd |

| strikePrice | string | false | The strike price is the predetermined price at which a put buyer can sell the underlying asset |

| optionType | string | false | Option Type (PE/CE). |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Request successful",

"optionChainDetails": [

{

"tradingSymbol": "TCS20JUN2800CE",

"exchange": "NFO",

"symbol": "64790_NFO",

"strikePrice": "2800.00",

"expiryDate": "25 Jun 2020",

"instrument": "OPTSTK",

"optionType": "CE",

"underLyingSymbol": "TCS",

"spotPrice": "2045.80",

"lastTradedPrice": "0.00",

"openInterest": "0",

"openInterestChange": "0",

"oichangePer": "0",

"volume": "0",

"bestBids": [

{

"number": "2",

"quantity": "88",

"price": "1575.55"

}

],

"bestAsks": [

{

"number": "2",

"quantity": "88",

"price": "1575.55"

}

]

}

]

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | OptionChain details retrived successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to retrieve scrip details. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| optionChainDetails | [object] | Scrips Details available for the provided search text. |

| tradingSymbol | string | Trading Symbol of the scrip. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| symbol | string | Symbol Code of the trading Symbol |

| strikePrice | string | The strike price is the predetermined price at which a put buyer can sell the underlying asset. |

| expiryDate | string | Shows expiry date of a trading symbol. |

| instrument | string | Instrument Name. |

| optionType | string | Option Type (PE/CE). |

| underLyingSymbol | string | Root symbol of TradingSymbol |

| spotPrice | string | Spot price. Applicable in case of Futures and Options |

| lastTradedPrice | string | Price at which last transaction / trade is done |

| openInterest | string | Open interest is the Number of existing contracts held by buyers or sellers for any market for any given day. |

| openInterestChange | string | It shows Open interest change in Number of contracts held for market |

| oichangePer | string | It will shows the change % based on Open Interest |

| volume | string | Limit amount of a security traded on the specific day |

| bestBids | [object] | Most frequent trading bids for BUY |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

| bestAsks | [object] | Most frequent trading asked for SELL |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

Future

Future Chain

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'e84ae32596c43f7d9260c9ece3d6b08e'

};

$.ajax({

url: 'https://api.stocknote.com/future/futureChain?searchSymbolName=TCS',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'e84ae32596c43f7d9260c9ece3d6b08e'

}

r = requests.get('https://api.stocknote.com/future/futureChain', params={

'searchSymbolName': 'TCS'

}, headers = headers)

print r.json()

GET /future/futureChain

This API is used to search futureChain for equity, derivatives, and commodity scripts based on the user-provided search symbol and exchange name.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| exchange | string | false | Name of the exchange.Valid exchanges values (NFO/MFO/CDS).If the user does not provide an exchange name, by default considered as NFO.For trading with CDS and MFO, exchange is mandatory. |

| searchSymbolName | string | true | Trading Symbol of the scrip to be searched |

| expiryDate | string | false | From date in yyyy-MM-dd |

Example responses

200 Response

{

"serverTime": "12/08/23 21:41:44",

"msgId": "128f4075-5113-46cb-8f0c-86f9a61ef306",

"status": "Success",

"statusMessage": "FutureChain details retrived successfully. ",

"futureChainDetails": [

{

"tradingSymbol": "TCS23AUGFUT",

"exchange": "NFO",

"symbol": "48404_NFO",

"expiryDate": "2023-08-31",

"instrument": "FUTSTK",

"underLyingSymbol": "TCS",

"spotPrice": "3448.80",

"lastTradedPrice": "3458.35",

"openInterest": "10646475",

"openInterestChange": "239575",

"oichangePer": "2.25",

"volume": "2129750",

"bestBids": [

{

"number": "1",

"quantity": "175",

"price": "3460.00"

},

{

"number": "2",

"quantity": "175",

"price": "3458.00"

},

{

"number": "3",

"quantity": "175",

"price": "3457.95"

},

{

"number": "4",

"quantity": "175",

"price": "3457.55"

},

{

"number": "5",

"quantity": "175",

"price": "3456.65"

}

],

"bestAsks": [

{

"number": "1",

"quantity": "175",

"price": "3461.00"

},

{

"number": "2",

"quantity": "175",

"price": "3461.90"

},

{

"number": "3",

"quantity": "175",

"price": "3462.00"

},

{

"number": "4",

"quantity": "175",

"price": "3462.50"

},

{

"number": "5",

"quantity": "350",

"price": "3462.65"

}

]

}

]

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | FutureChain details retrived successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to retrieve scrip details. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| futureChainDetails | [object] | Scrips Details available for the provided search text. |

| tradingSymbol | string | Trading Symbol of the scrip. |

| exchange | string | Name of the exchange.Valid exchanges values ( NFO/ MFO/ CDS).If the user does not provide an exchange name, by default considered as NFO.For trading with MFO and CDS, exchange is mandatory. |

| symbol | string | Symbol Code of the trading Symbol |

| expiryDate | string | Shows expiry date of a trading symbol. |

| instrument | string | Instrument Name. |

| underLyingSymbol | string | Root symbol of TradingSymbol |

| spotPrice | string | Spot price. Applicable in case of Futures and Options |

| lastTradedPrice | string | Price at which last transaction / trade is done |

| openInterest | string | Open interest is the Number of existing contracts held by buyers or sellers for any market for any given day. |

| openInterestChange | string | It shows Open interest change in Number of contracts held for market |

| oichangePer | string | It will shows the change % based on Open Interest |

| volume | string | Limit amount of a security traded on the specific day |

| bestBids | [object] | Most frequent trading bids for BUY |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

| bestAsks | [object] | Most frequent trading asked for SELL |

| number | string | Sequence number for Bid/Ask |

| quantity | string | Quantity asked for trading. |

| price | string | Price asked for trading. |

User Limits

User Limits

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/limit/getLimits',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/limit/getLimits'

,headers = headers)

print r.json()

GET /limit/getLimits

Gets the user cash balances, available margin for trading in equity and commodity segments.

Parameters

| Name | Type | Required | Description |

|---|

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Request successful",

"equityLimit": {

"grossAvailableMargin": "50000000000",

"payInToday": "0",

"notionalCash": "0",

"collateralMarginAgainstShares": "0",

"marginUsed": "27380.9",

"netAvailableMargin": "49999972619.1"

},

"commodityLimit": {

"grossAvailableMargin": "50000000000",

"payInToday": "0",

"notionalCash": "0",

"collateralMarginAgainstShares": "0",

"marginUsed": "27380.9",

"netAvailableMargin": "49999972619.1"

}

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Limits successfully retrieved. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Limits cannot be retrieve. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| equityLimit | object | none |

| grossAvailableMargin | string | Total amount of margins or balances available for trading. Opening balance for current day |

| payInToday | string | Current day deposited amount |

| notionalCash | string | Additional Limit that may or may not be given by RMS for Trading. |

| collateralMarginAgainstShares | string | Margin against shares offered by SAMCO to their clients for trading in stock and shares. |

| marginUsed | string | The amount deducted from opening balance for trading on the current day, and the amount blocked for creating a position when user places an order. |

| netAvailableMargin | string | Actual margin available with user for Trading after making all necessary adjustments. |

| commodityLimit | object | none |

| grossAvailableMargin | string | Total amount of margins or balances available for trading. Opening balance for current day |

| payInToday | string | Current day deposited amount |

| notionalCash | string | Additional Limit that may or may not be given by RMS for Trading. |

| collateralMarginAgainstShares | string | Margin against shares offered by SAMCO to their clients for trading in stock and shares. |

| marginUsed | string | The amount deducted from opening balance for trading on the current day, and the amount blocked for creating a position when user places an order. |

| netAvailableMargin | string | Actual margin available with user for Trading after making all necessary adjustments. |

Orders

Place Order

Code samples

var headers = {

'Content-Type':'application/json',

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/placeOrder',

method: 'post',

data: JSON.stringify(requestBody),

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Content-Type': 'application/json',

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.post('https://api.stocknote.com/order/placeOrder'

, data=json.dumps(requestBody)

, headers = headers)

print r.json()

POST /order/placeOrder

This API allows you to place an equity/derivative order to the exchange i.e the place order request typically registers the order with OMS and when it happens successfully, a success response is returned. Successful placement of an order via the API does not imply its successful execution. To be precise, under normal scenarios, the whole flow of order execution starting with order placement, routing to OMS and transfer to the exchange, order execution, and confirmation from exchange happen real time. But due to various reasons like market hours, exchange related checks etc. This may not happen instantly. So when an order is successfully placed the placeOrder API returns an orderNumber in response, and in scenarios as above the actual order status can be checked separately using the orderStatus API call.This is for Placing CNC, MIS and NRML Orders

Body parameter

requestBody={

"symbolName": "RELIANCE",

"exchange": "BSE",

"transactionType": "BUY",

"orderType": "L",

"quantity": "1",

"disclosedQuantity": "1",

"price": "1240.0",

"priceType": "LTP",

"marketProtection": " ",

"orderValidity": "DAY",

"afterMarketOrderFlag": "NO",

"productType": "MIS",

"triggerPrice": "0.00"

}

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| body | object | false | none |

| symbolName | string | true | Pass "name" in "symbolName" parameter for Equity Cash symbols and "Trading Symbol" for all the F&O contracts ('name' and 'tradingSymbol' is available in ScripMaster.csv). |

| exchange | string | true | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| transactionType | string | true | Transaction type should be BUY or SELL |

| orderType | string | true | Type of order. It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market |

| quantity | string | true | Quantity with which order is being placed |

| disclosedQuantity | string | true | If provided should be minimum of 10% of actual quantity |

| price | string | true | Price at which the order will be placed |

| priceType | string | true | Price type required to place an order. Valid price type - LTP/ATP , default is LTP. Applicable for BO orders only. |

| marketProtection | string | true | Percentage of MarketProtection required for ordertype MKT/SL-M to limit loss due to market price changes against the price with which order is placed. Default value is 3%. |

| orderValidity | string | true | Order validity can be DAY / IOC .Day is an order type which is valid for the whole trading day and stays pending till it is executed in respective trading day. IOC(Immediate Or Cancel) order type is where once the user punches the order, the order hits the exchange and if not executed immediately, the order stands cancelled |

| afterMarketOrderFlag | string | true | After Market Order Flag YES/NO |

| productType | string | true | Product Type of the order. It can be CNC (Cash and Carry)NRML (Normal),MIS (Intraday) |

| triggerPrice | string | false | The price at which an order should be triggered in case of SL, SL-M |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"orderNumber": "191206000000079",

"status": "Success",

"statusMessage": "MIS Order request placed successfully",

"exchangeOrderStatus": "complete",

"rejectionReason": "--",

"orderDetails": {

"pendingQuantity": "0",

"avgExecutionPrice": "1193.00",

"orderPlacedBy": "DV9999",

"tradingSymbol": "RELIANCE",

"triggerPrice": "0.00",

"exchange": "BSE",

"totalQuantity": "1",

"expiry": "--",

"transactionType": "BUY",

"productType": "MIS",

"orderType": "L",

"quantity": "1",

"filledQuantity": "1",

"orderPrice": "1240.00",

"filledPrice": "1240.0",

"exchangeOrderNo": "1565067682526005486",

"orderValidity": "DAY",

"orderTime": "12/12/2019 16:20:09"

}

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Order placed successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to place an Order. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| orderNumber | string | Unique Order identifier generated after placing an order which could be used for tracking order status |

| status | string | Status of the order. It would be success or failure |

| statusMessage | string | Order placement status Message |

| exchangeOrderStatus | string | Status of the order execution at Exchange side, Most common values are PENDING, COMPLETE, REJECTED, CANCELLED, and OPEN |

| rejectionReason | string | If an order is rejected, cause of order rejection which comes as user friendly textual description |

| orderDetails | object | none |

| pendingQuantity | string | Quantity which is in waiting state to be filled in a specific trade |

| avgExecutionPrice | string | Average price at which the quantities were bought/sold during the day |

| orderPlacedBy | string | Client code of the user who placed the order |

| tradingSymbol | string | Trading Symbol of the scrip. |

| triggerPrice | string | The price at which an order should be triggered in case of SL, SL-M. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| totalQuantity | string | Total Quantity |

| expiry | string | expiry date of trading symbol |

| transactionType | string | Type of the transaction, BUY / SELL. |

| productType | string | Product Type of order as placed by the user. It can be CNC (Cash and Carry),BO (Bracket Order),CO (Cover Order),NRML (Normal),MIS (Intraday). |

| orderType | string | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| quantity | string | Order Quantity as placed by the user |

| filledQuantity | string | Quantity which is filled in a specific trade. Can be less than or equal to the total quantity |

| orderPrice | string | Limit price entered at the time of placing the order. |

| filledPrice | string | Price at which exchange has filled the order |

| exchangeOrderNo | string | Order identifier at the exchange. |

| orderValidity | string | validity of the order |

| orderTime | string | Order placement time |

Place BO Order

Code samples

var headers = {

'Content-Type':'application/json',

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/placeOrderBO',

method: 'post',

data: JSON.stringify(requestBody),

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Content-Type': 'application/json',

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.post('https://api.stocknote.com/order/placeOrderBO'

, data=json.dumps(requestBody)

, headers = headers)

print r.json()

POST /order/placeOrderBO

This API allows you to place an equity/derivative order to the exchange i.e the place order request typically registers the order with OMS and when it happens successfully, a success response is returned. Successful placement of an order via the API does not imply its successful execution. To be precise, under normal scenarios, the whole flow of order execution starting with order placement, routing to OMS and transfer to the exchange, order execution, and confirmation from exchange happen real time. But due to various reasons like market hours, exchange related checks etc. This may not happen instantly. So when an order is successfully placed the placeOrder API returns an orderNumber in response, and in scenarios as above the actual order status can be checked separately using the orderStatus API call. This is for Placing BO Orders.

Body parameter

requestBody={

"symbolName": "RELIANCE",

"exchange": "NSE",

"transactionType": "BUY",

"orderType": "L",

"quantity": "1",

"disclosedQuantity": "1",

"price": "1240.0",

"priceType": "LTP",

"orderValidity": "DAY",

"productType": "BO",

"squareOffValue": "5",

"stopLossValue": "5",

"valueType": "Ticks",

"trailingStopLoss": "5"

}

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| body | object | false | none |

| symbolName | string | true | Pass "name" in "symbolName" parameter for Equity Cash symbols and "Trading Symbol" for all the F&O contracts ('name' and 'tradingSymbol' is available in ScripMaster.csv) |

| exchange | string | true | Name of the exchange.Valid exchanges values (NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with NFO, CDS and MCX, exchange is mandatory. BO orders not applicable to place in BSE exchange. |

| transactionType | string | true | Transaction type should be BUY or SELL |

| orderType | string | true | Type of order. It should be L- Limit Order |

| quantity | string | true | Quantity with which order is being placed |

| disclosedQuantity | string | true | If provided should be minimum of 10% of actual quantity |

| price | string | true | Price at which the order will be placed |

| priceType | string | true | Price type required to place an order. Valid price type - LTP/ATP , default is LTP. Applicable for BO orders only. |

| orderValidity | string | true | Order validity should be DAY .Day is an order type which is valid for the whole trading day and stays pending till it is executed in respective trading day. |

| productType | string | true | Product Type of the order. It can be BO (Bracket Order)) |

| squareOffValue | string | true | Price difference from entry price at which the order should be squared off to limit losses (eg: if Order price is 300. Profit target is 305. So target = 5). Applicable for BO orders only |

| stopLossValue | string | true | Stoploss price difference from the entry price at which the order should be squared off (eg: if Order price is 300. Stoploss target is 295. So stop loss = 5). Applicable for both BO & CO |

| valueType | string | true | ValueType required to place an Order. Applicable for both Stop Loss Value and Square off value. Valid value types - Absolute/Ticks. Default is Absolute.Applicable for BO orders only. |

| trailingStopLoss | string | true | Incremental value set as % of change from the market price. Trailing stop moves as the price moves up. but, if the price starts to fall, the stop loss does not move (For example, if you buy a stock at Rs 100 and set a trailing stop loss value of Rs 2. If the stock price moves up to say Rs 105, the trailing stop loss value also would move up to be Rs 103 and stays Rs 2 less than the current market price. But if the stock price starts to fall and becomes Rs 103, trailing stop loss order will become a market order. Applicable for BO orders only |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"orderNumber": "190726000001077",

"status": "Success",

"exchangeOrderStatus": "Executed",

"rejectionReason": "--",

"statusMessage": "BO Order request placed successfully",

"orderDetails": {

"pendingQuantity": "0",

"avgExecutionPrice": "1193.00",

"orderPlacedBy": "DV9999",

"tradingSymbol": "RELIANCE",

"triggerPrice": "0.00",

"exchange": "NSE",

"totalQuantity": "1",

"expiry": "--",

"transactionType": "BUY",

"productType": "BO",

"orderType": "L",

"quantity": "1",

"filledQuantity": "1",

"orderPrice": "1240.00",

"filledPrice": "1240.0",

"exchangeOrderNo": "1565067682526005486",

"orderValidity": "DAY",

"orderTime": "12/12/2019 16:20:09"

}

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | BO Order placed successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to place an BO Order. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| orderNumber | string | Unique Order identifier generated after placing an order which could be used for tracking order status |

| status | string | Status of the order. It would be success or failure |

| exchangeOrderStatus | string | Status of the order execution at Exchange side, Most common values are PENDING, COMPLETE, REJECTED, CANCELLED, and OPEN |

| rejectionReason | string | If an order is rejected, cause of order rejection which comes as user friendly textual description |

| statusMessage | string | Order placement status Message |

| orderDetails | object | none |

| pendingQuantity | string | Quantity which is in waiting state to be filled in a specific trade |

| avgExecutionPrice | string | Average price at which the quantities were bought/sold during the day |

| orderPlacedBy | string | Client code of the user who placed the order |

| tradingSymbol | string | Trading Symbol of the scrip. |

| triggerPrice | string | The price at which an order should be triggered in case of SL, SL-M. |

| exchange | string | Name of the exchange.Valid exchanges values (NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with NFO, CDS and MCX, exchange is mandatory. BO orders not applicable for BSE exchange. |

| totalQuantity | string | Total Quantity |

| expiry | string | expiry date of trading symbol |

| transactionType | string | Type of the transaction, BUY / SELL. |

| productType | string | Product Type of order as placed by the user is BO (Bracket Order) |

| orderType | string | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| quantity | string | Order Quantity as placed by the user |

| filledQuantity | string | Quantity which is filled in a specific trade. Can be less than or equal to the total quantity |

| orderPrice | string | Limit price entered at the time of placing the order. |

| filledPrice | string | Price at which exchange has filled the order |

| exchangeOrderNo | string | Order identifier at the exchange. |

| orderValidity | string | validity of the order |

| orderTime | string | Order placement time |

Place CO Order

Code samples

var headers = {

'Content-Type':'application/json',

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/placeOrderCO',

method: 'post',

data: JSON.stringify(requestBody),

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Content-Type': 'application/json',

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.post('https://api.stocknote.com/order/placeOrderCO'

, data=json.dumps(requestBody)

, headers = headers)

print r.json()

POST /order/placeOrderCO

This API allows you to place an equity/derivative order to the exchange i.e the place order request typically registers the order with OMS and when it happens successfully, a success response is returned. Successful placement of an order via the API does not imply its successful execution. To be precise, under normal scenarios, the whole flow of order execution starting with order placement, routing to OMS and transfer to the exchange, order execution, and confirmation from exchange happen real time. But due to various reasons like market hours, exchange related checks etc. This may not happen instantly. So when an order is successfully placed the placeOrder API returns an orderNumber in response, and in scenarios as above the actual order status can be checked separately using the orderStatus API call. This is for Placing CO Orders.

Body parameter

requestBody={

"symbolName": "RELIANCE",

"exchange": "BSE",

"transactionType": "BUY",

"orderType": "L",

"quantity": "1",

"disclosedQuantity": "1",

"price": "1240.0",

"orderValidity": "DAY",

"productType": "CO",

"triggerPrice": "1070.00"

}

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| body | object | false | none |

| symbolName | string | true | Pass "name" in "symbolName" parameter for Equity Cash symbols and "Trading Symbol" for all the F&O contracts ('name' and 'tradingSymbol' is available in ScripMaster.csv) |

| exchange | string | true | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| transactionType | string | true | Transaction type should be BUY or SELL |

| orderType | string | true | Type of order. It can be one of the following, MKT - Market Order,L- Limit Order |

| quantity | string | true | Quantity with which order is being placed |

| disclosedQuantity | string | true | If provided should be minimum of 10% of actual quantity |

| price | string | true | Price at which the order will be placed |

| orderValidity | string | true | Order validity should be DAY .Day is an order type which is valid for the whole trading day and stays pending till it is executed in respective trading day. |

| productType | string | true | Product Type of the order. It can be CO (Cover Order)) |

| triggerPrice | string | false | The price at which an order should be triggered |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"orderNumber": "190726000001077",

"status": "Success",

"exchangeOrderStatus": "Executed",

"rejectionReason": "--",

"statusMessage": "CO Order request placed successfully",

"orderDetails": {

"pendingQuantity": "0",

"avgExecutionPrice": "1193.00",

"orderPlacedBy": "DV9999",

"tradingSymbol": "RELIANCE",

"triggerPrice": "0.00",

"exchange": "BSE",

"totalQuantity": "1",

"expiry": "--",

"transactionType": "BUY",

"productType": "CO",

"orderType": "L",

"quantity": "1",

"filledQuantity": "1",

"orderPrice": "1240.00",

"filledPrice": "1240.0",

"exchangeOrderNo": "1565067682526005486",

"orderValidity": "DAY",

"orderTime": "12/12/2019 16:20:09"

}

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | CO Order placed successfully. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Failed to place an CO Order. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| orderNumber | string | Unique Order identifier generated after placing an order which could be used for tracking order status |

| status | string | Status of the order. It would be success or failure |

| exchangeOrderStatus | string | Status of the order execution at Exchange side, Most common values are PENDING, COMPLETE, REJECTED, CANCELLED, and OPEN |

| rejectionReason | string | If an order is rejected, cause of order rejection which comes as user friendly textual description |

| statusMessage | string | Order placement status Message |

| orderDetails | object | none |

| pendingQuantity | string | Quantity which is in waiting state to be filled in a specific trade |

| avgExecutionPrice | string | Average price at which the quantities were bought/sold during the day |

| orderPlacedBy | string | Client code of the user who placed the order |

| tradingSymbol | string | Trading Symbol of the scrip. |

| triggerPrice | string | The price at which an order should be triggered in case of SL, SL-M. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| totalQuantity | string | Total Quantity |

| expiry | string | expiry date of trading symbol |

| transactionType | string | Type of the transaction, BUY / SELL. |

| productType | string | Product Type of order as placed by the user is CO (Cover Order) |

| orderType | string | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| quantity | string | Order Quantity as placed by the user |

| filledQuantity | string | Quantity which is filled in a specific trade. Can be less than or equal to the total quantity |

| orderPrice | string | Limit price entered at the time of placing the order. |

| filledPrice | string | Price at which exchange has filled the order |

| exchangeOrderNo | string | Order identifier at the exchange. |

| orderValidity | string | validity of the order |

| orderTime | string | Order placement time |

Get Order Status

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/getOrderStatus?orderNumber=190707000000004',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/order/getOrderStatus', params={

'orderNumber': '190707000000004'

}, headers = headers)

print r.json()

GET /order/getOrderStatus

Get status of an order placed previously. This API returns all states of the orders,but not limited to open, pending, and partially filled ones.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| orderNumber | string | true | Order Number for which the user wants to check the order status |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"orderNumber": "190722000000243",

"orderStatus": "Success",

"statusMessage": "Requested MIS Order placed successfully",

"orderDetails": {

"pendingQuantity": "0",

"avgExecutionPrice": "1193.00",

"orderPlacedBy": "DV9999",

"tradingSymbol": "RELIANCE",

"triggerPrice": "0.00",

"exchange": "BSE",

"totalQuantity": "1",

"expiry": "--",

"transactionType": "BUY",

"productType": "MIS",

"orderType": "L",

"quantity": "1",

"filledQuantity": "1",

"orderPrice": "1240.00",

"filledPrice": "1240.0",

"exchangeOrderNo": "1565067682526005486",

"orderValidity": "DAY",

"orderTime": "12/12/2019 16:20:09"

}

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Order status successfully retrived. |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Servsr Error. Failed to retrive OrderStatus. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| orderNumber | string | Unique number generated at the exchange while placing an order |

| orderStatus | string | Status of the order at Exchange side, Most common values are PENDING, COMPLETE, REJECTED, CANCELLED, and OPEN |

| statusMessage | string | Status Message of the order |

| orderDetails | object | none |

| pendingQuantity | string | Quantity which is in waiting state to be filled in a specific trade |

| avgExecutionPrice | string | Average price at which the quantities were bought/sold during the day |

| orderPlacedBy | string | Client code of the user who placed the order |

| tradingSymbol | string | Trading Symbol of the scrip. |

| triggerPrice | string | The price at which an order should be triggered in case of SL, SL-M. |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| totalQuantity | string | Total Quantity |

| expiry | string | expiry date of trading symbol |

| transactionType | string | Type of the transaction, BUY / SELL. |

| productType | string | Product Type of order as placed by the user. It can be CNC (Cash and Carry),BO (Bracket Order),CO (Cover Order),NRML (Normal),MIS (Intraday). |

| orderType | string | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| quantity | string | Order Quantity as placed by the user |

| filledQuantity | string | Quantity which is filled in a specific trade. Can be less than or equal to the total quantity |

| orderPrice | string | Limit price entered at the time of placing the order. |

| filledPrice | string | Price at which exchange has filled the order |

| exchangeOrderNo | string | Order identifier at the exchange. |

| orderValidity | string | validity of the order |

| orderTime | string | Order placement time |

Order Book

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/orderBook',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/order/orderBook'

, headers = headers)

print r.json()

GET /order/orderBook

Orderbook retrieves and displays details of all orders placed by the user on a specific day. This API returns all states of the orders, namely, open, pending, rejected and executed ones.

Parameters

| Name | Type | Required | Description |

|---|

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "Request successful",

"orderBookDetails": [

{

"orderNumber": "191206000000079",

"exchange": "BSE",

"tradingSymbol": "RELIANCE",

"symbolDescription": "RELIANCE INDUSTRIES LTD.",

"transactionType": "BUY",

"productCode": "MIS",

"orderType": "L",

"orderPrice": "1560.15",

"quantity": "13",

"disclosedQuantity": "1",

"triggerPrice": "1090.00",

"marketProtection": "3",

"orderValidity": "DAY",

"orderStatus": "Complete",

"orderValue": "20281.95",

"instrumentName": "NA",

"orderTime": "06-Dec-2019 13:47:04",

"userId": "DV99999",

"filledQuantity": "13",

"fillPrice": "1560.15",

"averagePrice": "1560.15",

"unfilledQuantity": "0",

"exchangeOrderId": "1575608622401000995",

"rejectionReason": "NA",

"exchangeConfirmationTime": "06-Dec-2019 14:14:47",

"cancelledQuantity": "0",

"referenceLimitPrice": "0.00",

"coverOrderPercentage": "0.00",

"orderRemarks": "--",

"exchangeOrderNumber": "1575608622401000995",

"symbol": "52310_NFO",

"displayStrikePrice": "0.00",

"displayNetQuantity": "10",

"status": "complete",

"exchangeStatus": "complete",

"expiry": "--",

"pendingQuantity": "0",

"instrument": "--",

"scripName": "--",

"totalQuanity": "13",

"optionType": "--",

"orderPlaceBy": "DV99999",

"lotQuantity": "1",

"parentOrderId": "200824000050316"

}

]

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | Order book details successfully retrieved |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. Order book details cannot be retrieved. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| orderBookDetails | [object] | List of all orders with details during the day |

| orderNumber | string | Unique Order identifier generated after placing an order |

| exchange | string | Name of the exchange.Valid exchanges values (BSE/ NSE/ NFO/ MCX/ CDS).If the user does not provide an exchange name, by default considered as NSE.For trading with BSE, NFO, CDS and MCX, exchange is mandatory. |

| tradingSymbol | string | Trading Symbol of the scrip. |

| symbolDescription | string | Scrip description |

| transactionType | string | Type of the transaction, BUY / SELL. |

| productCode | string | Product Type of order as placed by the user. It can be CNC (Cash and Carry),BO (Bracket Order),CO (Cover Order),NRML (Normal),MIS (Intraday). |

| orderType | string | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| orderPrice | string | Total price of a particular order |

| quantity | string | Total Quantity as placed by the user |

| disclosedQuantity | string | If provided should be minimun of 10% of actual quantity. |

| triggerPrice | string | The price at which an order should be triggered in case of SL, SL-M. |

| marketProtection | string | Percentage of MarketProtection required for ordertype MKT/SL-M to limit loss due to market price changes against the price with which order is placed. Default value is 3%. |

| orderValidity | string | Order validity can be DAY / IOC |

| orderStatus | string | Status of the order at Exchange side, either executed successfully or pending or rejected |

| orderValue | string | Value of the order |

| instrumentName | string | Name of the instrument |

| orderTime | string | Order placement time |

| userId | string | The client Code provided to you by SAMCO after opening an account. |

| filledQuantity | string | Quantity which is filled in a specific trade. Can be less than or equal to the total quantity |

| fillPrice | string | Price at which exchange has filled the order |

| averagePrice | string | Average trading price of the equity |

| unfilledQuantity | string | Quantity which is not filled in a partially filled order. Can be less than or equal to the total quantity |

| exchangeOrderId | string | Unique Order identifier generated from exchange |

| rejectionReason | string | If order is rejected, Cause of order Rejection |

| exchangeConfirmationTime | string | Order confirmation time at exchange |

| cancelledQuantity | string | cancelled quantity for partial cancelled orders |

| referenceLimitPrice | string | Limit Price reference |

| coverOrderPercentage | string | Percentage of cover order |

| orderRemarks | string | Remarks about order |

| exchangeOrderNumber | string | Unique Order identifier generated after placing an order |

| symbol | string | symbol about stock |

| displayStrikePrice | string | Shows the strick price |

| displayNetQuantity | string | Display the limit quantity of order |

| status | string | Status will display Executed/Pending/Rejected |

| exchangeStatus | string | ExchangeStatus will display Executed/Pending/Rejected |

| expiry | string | shows ExpiryDate of the stock |

| pendingQuantity | string | PendingQuantity will show pending quantity stock |

| instrument | string | Instrument is about the type of stock. FUT/OPT |

| scripName | string | Name of the scrip |

| totalQuanity | string | Total Quantity |

| optionType | string | Option Type (PE/CE). |

| orderPlaceBy | string | Client code of the user who placed the order |

| lotQuantity | string | lotQuantity represents the number of contracts contained in one derivative security.Applicable for F & O |

| parentOrderId | string | order Id of the parent order(it is applicable for only BO/CO orders) |

TriggerOrders

Code samples

var headers = {

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/getTriggerOrders?orderNumber=190707000000004',

method: 'get',

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.get('https://api.stocknote.com/order/getTriggerOrders', params={

'orderNumber': '190707000000004'

}, headers = headers)

print r.json()

GET /order/getTriggerOrders

This API allows you to get the trigger order numbers in case of BO and CO orders so that their attribute values can be modified for BO orders, it will give the order identifiers. For Stop loss leg and target leg. Similarly for CO orders, it will return order identifier of stop loss leg only. Using the order identifier, the user would be able to modify the order attributes using the modifyOrder API. Refer modifyOrder API documentation for the parameters details.

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| orderNumber | string | true | Order Number for which the user wants to check the order status |

Example responses

200 Response

{

"serverTime": "12/12/19 16:20:11",

"msgId": "786cdd94-2fc9-4c38-8f14-672ec64dd032",

"status": "Success",

"statusMessage": "SubOrder details retrieved successfully.",

"triggerOrders": [

{

"stopLossOrderNo": "191219000000063",

"orderStatus": "Complete",

"orderPrice": "351.20",

"triggerPrice": "331.20"

}

]

}

Responses

| Status | Meaning | Description |

|---|---|---|

| 200 | OK | SubOrder details successfully retrieved |

| 400 | Bad Request | Input validation Failed. Check the validation errors in response object. |

| 500 | Internal Server Error | Server Error. BO/CO SubOrder details cannot be retrieved. |

Response Schema

Status Code 200

| Name | Type | Description |

|---|---|---|

| serverTime | string | Time at Server. |

| msgId | string | This is a unique identifier for every request into the system. Please quote this identifier to the support team if you face issues with the API request. |

| status | string | Response status. Can be Success or Failure |

| statusMessage | string | status Message |

| triggerOrders | [object] | Trigger order Details available for the provided OrderNumber. |

| stopLossOrderNo | string | Unique Order identifier generated from exchange |

| orderStatus | string | Status of the order at Exchange side, either executed successfully complete or trigger pending or cancelled |

| orderPrice | string | price of a particular order |

| triggerPrice | string | The price at which an order should be triggered |

Modify Order

Code samples

var headers = {

'Content-Type':'application/json',

'Accept':'application/json',

'x-session-token':'c5c81c20f0fe81ceb45f93d3621d0938'

};

$.ajax({

url: 'https://api.stocknote.com/order/modifyOrder/{orderNumber}',

method: 'put',

data: JSON.stringify(requestBody),

headers: headers,

success: function(data) {

console.log(JSON.stringify(data));

},

error : function(error){

console.log(error);

}

})

import requests

headers = {

'Content-Type': 'application/json',

'Accept': 'application/json',

'x-session-token': 'c5c81c20f0fe81ceb45f93d3621d0938'

}

r = requests.put('https://api.stocknote.com/order/modifyOrder/{orderNumber}'

, data=json.dumps(requestBody)

, headers = headers)

print r.json()

PUT /order/modifyOrder/{orderNumber}

User would be able to modify some attributes of an order as long as it is with open/pending status in system. For modification order identifier is mandatory. With order identifier you need to send the optional parameter(s) which needs to be modified. In case the optional parameters aren't sent, the default will be considered from the original order. Modifiable attributes include quantity, Order Type (L,MKT, SL,SL-M). This API cannot be used for modifying attributes of an executed/rejected/cancelled order. Only the attribute that needs to be modified should be sent in the request alongwith the Order Identifier.

Body parameter

requestBody={

"orderType": "L",

"quantity": "3",

"disclosedQuantity": "1",

"orderValidity": "DAY",

"price": "1240.00",

"triggerPrice": "1070.00",

"parentOrderId": "190707000000004",

"marketProtection": "5"

}

Parameters

| Name | Type | Required | Description |

|---|---|---|---|

| orderNumber | string | true | Unique Order identifier of the order which needs to be modified |

| body | object | false | Type of order. MKT - Market Order,L - Limit Order, SL - Stop Loss Limit, SL-M - Stop Loss Market |

| orderType | string | false | Type of order user has placed . It can be one of the following, MKT - Market Order,L- Limit Order,SL - Stop Loss Limit,SL-M - Stop loss market. |

| quantity | string | false | Quantity of the order user wants to modify |